Happy Friday!

Happy Mother’s Day to all moms this weekend!

Stocks rise as unemployment claims increase amid signs of a cooling job market and hopes for slowing inflation. In a historical rarity, the services sector contracts as the manufacturing sector expands. Mammoth, the world’s largest vacuum, sucks more carbon dioxide out of the atmosphere. It’s the end of the road for the Chevy Malibu.

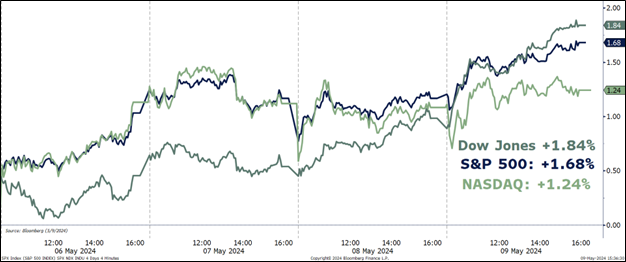

#1 – Weekly Market Recap – Stocks appear poised to end the week on a positive note. If the Dow Jones Industrial Average ends the day positive, it will mark its eighth consecutive day of gains – which hasn’t happened since December.

Through Thursday’s close, the Dow Jones Industrial Average lead the way up +1.84% for the week while the S&P 500 increased +1.68%, crossing the 5,200 level for the first time since April 9th. The Nasdaq Composite also gained +1.24%.

On Thursday, the market displayed indications of a broadening rally, notably the real estate and utility sectors taking the performance lead.

Investors appeared to have found solace in signs of a weakening jobs market which could lead to slowing inflation – the exact ingredients the Federal Reserve needs to start cutting interest rates.

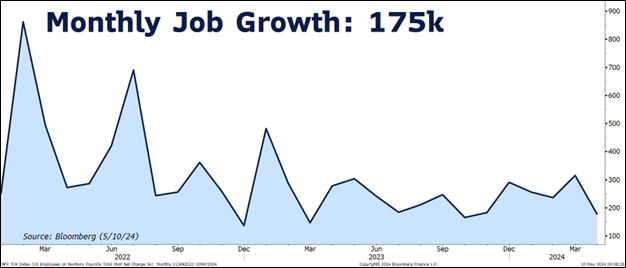

#2 – Declining Labor Landscape – The Department of Labor released data yesterday that raises concerns for the US labor market.

Initial filings for unemployment benefits surged to their highest level since August 2023, showing signs that a once-robust employment market is cooling.

Initial jobless claims for April increased by +22,000 to 231,000, significantly surpassing Bloomberg economists’ projections of 212,000. The spike, coupled with a rise in the four-week moving average to 215,000, the highest since February, suggests a shift unfolding in the US employment landscape.

The latest figures follow a disappointing April jobs report, which saw only 175,000 new jobs added for the month, falling short of analysts’ expectations of 240,000 and fueling investor speculation for potential interest rate cuts.

Several factors contributed to April’s uptick in unemployment claims. Before seasonal adjustments, initial applications rose by nearly +20,000. New York jobless claims accounted for ½ of the increase and California experienced a surge in jobless applications following the $20 minimum wage for fast-food workers implemented on April 1, 2024.

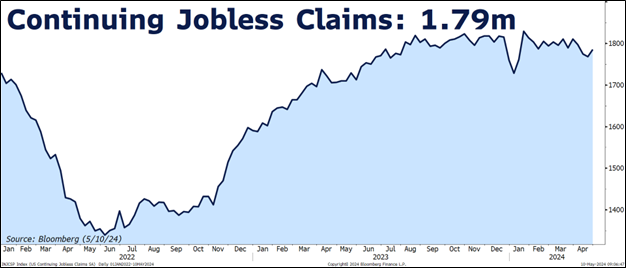

Continuing claims, which represent the number of people receiving unemployment benefits, rose to 1.79 million for the week ending April 27 – the highest over the past month.

The rise in unemployment claims comes as investors await a sign from the Federal Reserve as to when the time is right to cut interest rates. Continued deterioration in the labor market could force the Federal Reserve to entertain cutting interest rates even if inflation remains higher than the Fed’s 2% target.

Source: New York Post

#3 – Manufacturing vs Services – US economic growth may be changing according to new data released by the Institute for Supply Management (ISM).

The ISM’s “Purchasing Managers Index” (PMI), which measures business activity across the US economy, showed the services sector contracting in April for the first time in 15 months. Conversely, the manufacturing sector ended an 18-month contraction in March.

The services sector (light blue line in the chart above), accounts for roughly 2/3rds of the US economy and has been a key driver of US growth over the past 2 years. Meanwhile, the manufacturing sector, which is 1/3rd of the US economy, has been in contraction.

As shown in the chart above, it is a historical rarity to have the services sector in expansion territory (above 50 represented by the dashed red line), the manufacturing sector in contraction territory (below 50), and then the two coming together at a neutral 50 reading. In fact, this has never occurred since the data started in 1997!

What is the significance of this data?

At DSG Advisors, we believe that the deterioration in the services sector reflects a stretched US consumer suffering under persistently high prices caused by inflation, high interest rates, and a weakening labor market.

We applaud the recent strength in the manufacturing sector which we attribute, in part, to US manufacturing “onshoring” post pandemic (including billions of stimulus dollars provided to build semiconductor plants). However, we recognize that it would take a dramatic increase in manufacturing activity to “carry the load” for US economic growth as the manufacturing sector is just 1/3rd of the US economic activity.

We expect the next few months to be critical in determining if the services and manufacturing sectors meeting at 50 (neither expansion or contraction) is just a data oddity, or if it marks the beginning of a shift in economic output.

We find it noteworthy that contractionary services data historically does not portend well for the US economy. Specifically, the services PMI has experienced sustained periods of contraction on just 3 occurrences over the last 25 years: 2001, 2008-2009, and 2020. During each of those previous occurrences, the US entered a recession.

#4 – World’s Largest Vacuum – The world’s largest vacuum began operating this week in Iceland.

We first wrote about Icelandic “carbon sucking vacuums” back in October 2021 when we introduced our readers to Orca, the world’s largest “direct air carbon capture facility” (DAC) created by the Swiss firm Climeworks. At the time, we wrote how Orca would remove 10 metric tons of CO2 per day – the equivalent emissions of 800 US cars per year.

Climeworks introduced an even larger DAC on Wednesday. Dubbed “Mammoth,” the plant is 10 times larger than Orca. At full operational capacity, Mammoth is projected to remove approximately 100 metric tons of CO2 per day, the equivalent of 7,800 US cars per year.

Carbon dioxide emissions are a significant contributor to global warming and carbon dioxide levels in the Earth’s atmosphere reached a new record high in 2023.

DAC uses chemical reactions to pull CO2 out of the air. The separated CO2 can then be permanently stored deep underground or converted into products. In collaboration with Icelandic company Carbfix, Climeworks plans to transport the carbon captured by Mammoth underground so that it will naturally transform into stone– effectively permanently locking up the carbon.

Carbon removal technologies, however, are not without controversy. Critics say the technology is costly, it requires significant energy inputs, and lacks proven scalability. Additionally, some climate advocates say that focusing on carbon removal may divert attention and resources away from reducing our reliance on fossil fuels.

Although DACs are a creative way to remove CO2 from the atmosphere, their current impact on the world’s CO2 levels appears minor. With roughly 15 million new vehicles sold in the US last year, removing the equivalent carbon emissions of 7,800 vehicles is a noteworthy start, but much more needs to occur to reduce global CO2 levels.

Source: Business Standard

Source: Department of Energy

#5 – Goodbye Chevy Malibu – Chevrolet Malibu, the car that General Motors introduced to America in 1964, is headed for the scrap yard.

General Motors reported this week that after a 60-year run, it is ending production of the Malibu to focus on electric and hybrid vehicles. Over the 60 years, GM sold over 10 million Malibus,

The midsize sedan was once the top-selling segment in the US, but sales began to decline in the early 2000s as Americans gravitated toward SUV and pickup trucks. According to Motorintelligence.com, midsized car sales made up only 8% of US new vehicle sales in 2023…falling from 22% as recently as 2007. Full-size pickups from Ford, Chevrolet and Ram are currently the top selling vehicles in America.

General Motor’s Kansas City factory will stop producing the Malibu in November. The plant will then undergo a $390 million retooling to begin production of an updated Bolt, Chevrolet’s small electric car, in late 2025.

Say goodbye to a classic American car!

Source: AP News

Have a great weekend!

Denver & the DSGCA Team